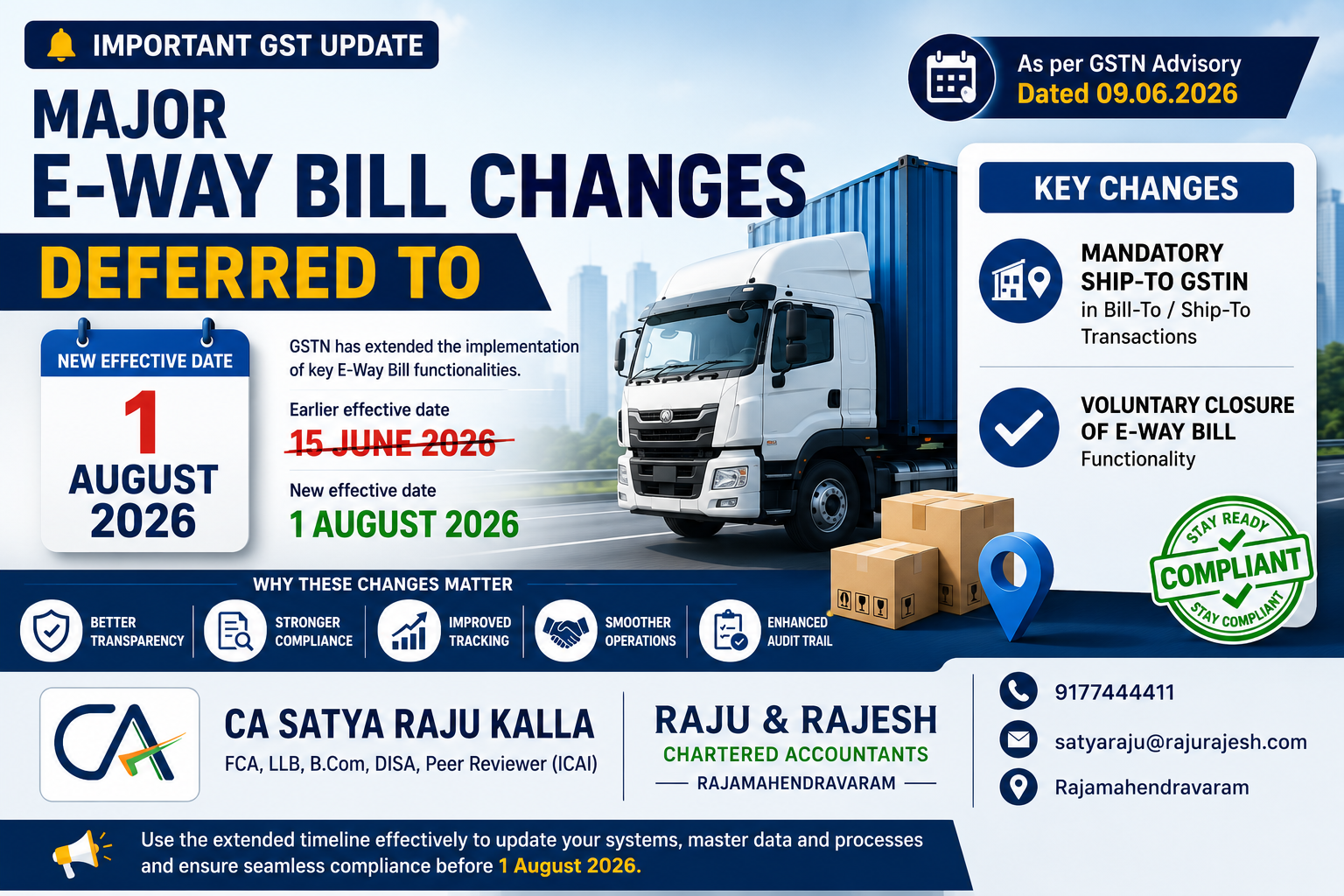

Major E-Way Bill Changes Deferred to 1 August 2026: What Businesses Need to Know

The Goods and Services Tax Network (GSTN) has announced an extension in the implementation timeline for two important E-Way Bill functionalities that were originally scheduled to become effective from 15 June 2026. Based on representations received from trade, industry, ERP providers, and other stakeholders, GSTN has decided to defer the implementation date to 1 August 2026.

The extension provides businesses additional time to update their systems, complete testing, revise master data, and ensure operational readiness before the new requirements become mandatory.

Background of the GSTN Advisory

GSTN had earlier announced the introduction of the following functionalities in the E-Way Bill system:

- Mandatory capture of Ship-To GSTIN in Bill-To/Ship-To transactions.

- Voluntary Closure of E-Way Bill functionality.

These changes were initially proposed to take effect from 15 June 2026. However, after considering requests from industry participants regarding ERP readiness, API integration, system modifications, and data updation requirements, GSTN has postponed the implementation date.

The revised effective date is now 1 August 2026.

Why These Changes Matter

The E-Way Bill system has become one of the most important compliance tools under GST. Tax authorities increasingly use E-Way Bill data for:

-

Verification of movement of goods

-

Detection of fake invoicing

-

Matching of e-Invoice and GST return data

Need help with this? Talk to RAJU & RAJESH → -

Identification of tax evasion

-

Tracking of supply chain transactions

The latest changes are intended to improve the quality and reliability of information available on the E-Way Bill portal.

1. Mandatory "Ship-To GSTIN" in Bill-To / Ship-To Transactions

Existing Practice

In many business transactions, the invoice is raised on one party while goods are delivered to another location.

Example:

-

Manufacturer issues invoice to Dealer A.

-

Goods are directly delivered to Customer B.

Such transactions are commonly known as:

Bill-To / Ship-To Transactions

Under the earlier system, many taxpayers either left the Ship-To GSTIN field blank or did not accurately capture the actual consignee's GSTIN.

New Requirement from 01 August 2026

Where goods are delivered to a registered recipient, the Ship-To GSTIN must now be mandatorily reported while generating the E-Way Bill.

Where goods are delivered to an unregistered person, taxpayers must mention:

URP (Unregistered Person)

instead of leaving the field blank.

Illustration

Scenario

ABC Manufacturers, Hyderabad

Invoice Raised To:

XYZ Traders, Vijayawada

Goods Delivered To:

PQR Industries, Guntur

E-Way Bill Reporting

Bill-To GSTIN:

GSTIN of XYZ Traders

Ship-To GSTIN:

GSTIN of PQR Industries

This will enable GST authorities to identify the actual destination and recipient of goods.

Benefits of Mandatory Ship-To GSTIN

Better Traceability

Authorities can track the actual movement of goods more accurately.

Reduction in Fake Transactions

Misuse of Bill-To / Ship-To arrangements for tax evasion can be minimized.

Improved Data Matching

Helps in reconciliation between:

-

E-Invoice

-

E-Way Bill

-

GST Returns

-

Actual Delivery

Stronger Audit Trail

Creates a complete chain of documentation from supplier to final recipient.

Businesses Most Affected

The following sectors frequently use Bill-To / Ship-To transactions:

-

Manufacturing companies

-

Trading businesses

-

Distributor networks

-

Warehousing operations

-

E-commerce sellers

-

FMCG businesses

-

Pharmaceutical companies

-

Logistics operators

Such businesses should immediately review their dispatch procedures.

2. Introduction of E-Way Bill Closure Facility

What is the New Feature?

GSTN has introduced a facility to formally close an E-Way Bill after successful delivery of goods.

Earlier, after delivery there was no mechanism to indicate that transportation had been completed.

The new closure facility fills this gap.

Who Can Close an E-Way Bill?

The facility can be used by:

-

Supplier

-

Recipient

-

Transporter

-

Driver or authorized person linked through registered mobile number

Benefits of E-Way Bill Closure

Better Record Management

Completed transactions can be formally marked as closed.

Reduced Compliance Risks

Eliminates confusion regarding completed and pending consignments.

Enhanced Monitoring

Businesses can easily distinguish between active and completed deliveries.

Improved Internal Controls

Useful for logistics and inventory management systems.

Important Time Limit

The closure facility can generally be used:

-

On the date of delivery, or

-

On the next day after delivery

Businesses should ensure prompt action to utilize this feature effectively.

3. ERP and Software Changes Required

Organizations using:

- Tally

-

Busy

-

Marg

-

Custom ERP Solutions

must update their systems before 01 Aug 2026

Required changes may include:

-

Addition of Ship-To GSTIN field

-

Validation controls

-

Updated EWB APIs

-

Closure functionality integration

-

Workflow modifications

Failure to update systems may result in E-Way Bill generation failures.

Compliance Checklist Before 01 August 2026

Businesses should complete the following activities:

Review Existing Bill-To / Ship-To Transactions

Identify all business processes involving different billing and delivery locations.

Update Customer Master Data

Ensure Ship-To GSTIN information is available and accurate.

Modify ERP Systems

Configure mandatory validation for Ship-To GSTIN.

Train Staff

Educate:

-

Accounts teams

-

Dispatch teams

-

Logistics staff

-

GST compliance personnel

Test E-Way Bill Generation

Perform trial runs before implementation.

Update SOPs

Revise internal documentation and compliance procedures.

Consequences of Non-Compliance

Failure to comply may lead to:

-

Inability to generate E-Way Bills

-

Delays in dispatch of goods

-

Transportation disruptions

-

Increased GST scrutiny

-

Potential penalties under GST law

Therefore, businesses should treat these changes as an important compliance requirement rather than a mere system update.

Practical Advice for Taxpayers

As Chartered Accountants and GST consultants, we recommend that businesses immediately conduct a review of:

-

Customer master records

-

Delivery location details

-

ERP configurations

-

Dispatch workflows

-

Logistics documentation

The sooner these changes are implemented, the smoother the transition will be after 01 August 2026

Conclusion

GSTN has deferred the implementation of the mandatory Ship-To GSTIN requirement and the Voluntary E-Way Bill Closure facility from 15 June 2026 to 1 August 2026. The extension provides valuable time for businesses, ERP providers, and GST professionals to complete system upgrades, testing, and process improvements.

Taxpayers should use this additional time wisely and ensure complete readiness before the revised implementation date to avoid operational and compliance challenges.

CA SATYA RAJU KALLA

FCA, LLB, B.Com, DISA, Peer Reviewer (ICAI)

RAJU & RAJESH

Chartered Accountants

Rajamahendravaram

📞 9177444411

📧 satyaraju@rajurajesh.com

Have Questions? We're Here to Help

Get expert advice from RAJU & RAJESH. Reach out to discuss your requirements.